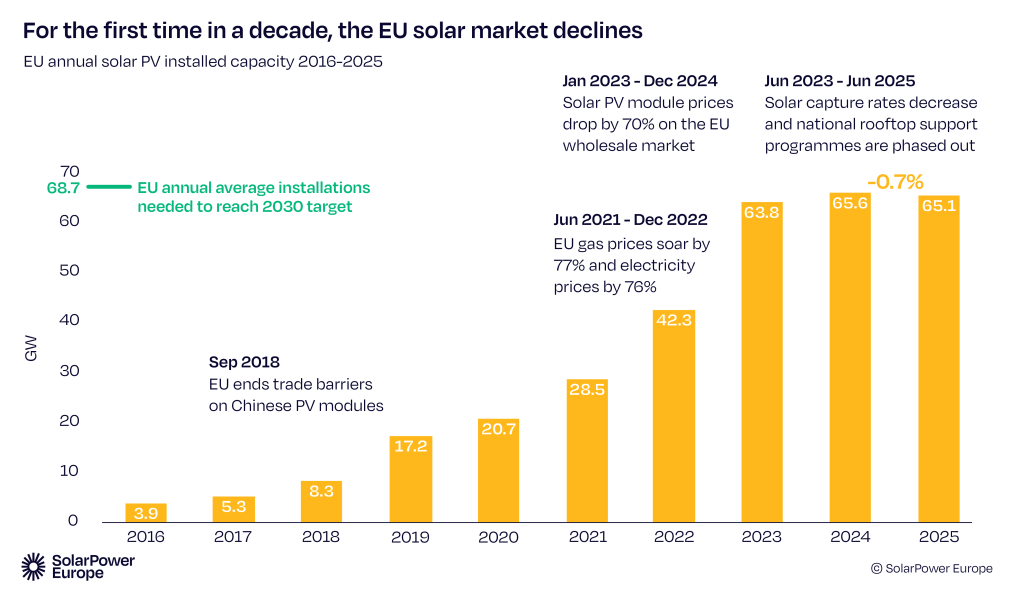

According to a report from SolarPower Europe, the European Union’s solar power boom has faded, with annual installations contracting for the first time since 2016.

The EU installed 65.1GW of solar capacity in 2025, marking a 0.7% decline from the 65.6GW installed the previous year.

Despite the downturn, the bloc surpassed a mid-decade milestone, reaching an estimated 406GW of total installed solar capacity across the EU by the end of the year, exceeding the 400GW target set in the 2022 EU Solar Strategy.

However, the slowdown is projected to continue through 2026 and 2027, with the annual installation returning to 2025 levels only around 2030, with roughly 67GW. This trajectory suggests the EU will fall short of its ambitious 750GW solar target for 2030.

“The number may seem small, but the symbolism is big,” said Walburga Hemetsberger, CEO of SolarPower Europe.

“This interruption in solar market growth comes at a pivotal moment when acceleration is essential. Solar is now delivering for Europe; 13% of Europe’s electricity was solar powered in 2025. In June we provided the most power out of all other sources in the EU.”

Hemetsberger added that it is “critical that policymakers now implement robust frameworks for electrification, system flexibility, and energy storage to ensure solar leads Europe’s energy transition for the rest of this decade.”

The market faltering is attributed to several factors, including an uncertain post-energy crisis environment that has led to cuts in rooftop support schemes and a perceived softening of energy price pressure on households.

Home rooftop solar, which was responsible for 28% of EU installed capacity in 2023, dropped significantly to account for only 14% in 2025.

In a segment shift, solar farms accounted for over 50% of installed solar capacity for the first time. However, this standalone solar segment faces increasing challenges to profitability, with a rising number of negative pricing hours reducing revenues.

Report highlights:

- Germany and Spain retained their positions as the EU’s largest, driven by utility-scale projects.

- France overtook Italy for the third-largest capacity, propelled by strong commercial and utility-scale expansion.

- Italy’s rooftop sector contracted following the phase-out of support schemes.

- Romania and Bulgaria entered the top 10 for the first time.

- The Netherlands’ ranking dropped significantly.

- Half of the top ten markets – Italy, Poland, Greece, the Netherlands, and Portugal – installed less solar in 2025 than in 2024.

Addressing common EU-level barriers, the report’s policy recommendations focus on redefining energy security around renewable sources, adopting a comprehensive strategy for flexibility, improving permitting procedures, boosting the rooftop solar market, and making solar supply chains more sustainable.

[Graph credit: SolarPower Europe]

Also in the news:

3,000 Solar professionals set to gather in Verona for the debut of Solar & Storage Live Italia, 8-9 October 2025 in Verona

Terrapinn and Veronafiere announce Solar & Storage Live Italia – Italy’s most exciting solar and energy storage exhibition, set to debut in Verona, 8-9 October 2025

3,000 Solar professionals set to gather in Verona for the debut of Solar & Storage Live Italia, 8-9 October 2025 in Verona

Terrapinn and Veronafiere announce Solar & Storage Live Italia – Italy’s most exciting solar and energy storage exhibition, set to debut in Verona, 8-9 October 2025

Spotlight on solar excellence: The Solar & Storage Live Awards reveals 2025 shortlist

Spotlight on solar excellence: The Solar & Storage Live Awards reveals 2025 shortlist